Advertisements

But after all, what is revolving credit and how does this rate negatively impact the consumer's pocket? Want to know how to get out of this trap? Read the text until the end and learn everything about how revolving interest works.

The main factor in Brazilian people's debt is credit cards, did you know that?

According to the Consumer Debt and Default Survey – carried out by the National Confederation of Commerce – and published in an article by CNN Brasil – the average number of indebted people is 70.9% in 2021.

But that's not all, the research also reveals the main "villain" in this situation, which is the credit card. According to the survey, our beloved card represents 82.6% in the "indebtedness factor" category.

And, no wonder! After all, the last revolving interest rate reached 346.1% per year. Despite this, you don't need to leave your financial ally aside, however, all care is essential.

Want to know everything about revolving credit so you don't fall into this trap and get out of it? Check out what you'll find out in this reading:

- What is revolving credit?

- How does credit card revolving payment work?

- How much is the interest on revolving credit?

- 5 tips on how to get out of your credit card revolving debt.

What is revolving credit?

Also known as the “snowball effect”, revolving credit is actually an “emergency credit”, available to the customer when they are unable to pay the bill in full.

In other words, the fee is charged whenever the consumer pays an amount below the total shown on the invoice.

In this way, it is as if the difference between the full amount and the amount paid were transformed into a “loan”, but with very high interest. In other words, the consumer pays a fee on a certain amount that he/she was unable to pay by the due date.

Phew, so if something unexpected happens financially, I have some security?

In practice, this is not exactly how it happens, since this is one of the main reasons for debt. And surely you have already experienced a “snowball” situation?

Debt on debt and interest on interest. Tell me if that's not true?

How does credit card revolving payment work?

Surely, our readers are super curious to know How does credit card revolving payment work? And it’s no wonder, after all, knowledge is power.

In short, as you have already seen in the previous topic, revolving credit or minimum invoice payment is an extra credit offered to the customer so that they do not fall into debt with the bank.

Therefore, the remaining amount and any interest due are charged on the following month's bill. However, on the “second bill” the consumer cannot use the revolving credit again. In this case, the existing option is to pay in installments.

Let's say, for example, that you have a debt of R$1,000.00 on your credit card, due on date X. The day arrives, something unexpected happens and you can't pay it all. But you still have R$1,500.00 available in your wallet for payment.

This amount is used to pay the bill and the remainder of the debt, R$$500.00, is charged by the bank the following month, with the revolving interest rate agreed upon at the time of joining.

The next month has arrived, if you are able to pay the bill in full the debt is paid off. However, if this is not possible, it is not possible to pay the minimum amount again, but you can use the option of installment payment of the credit card bill.

How much is the interest on revolving credit?

At this initial stage, it is extremely important to be aware of the following situation: Within the credit market, revolving interest rates are among the highest.

Furthermore, since 2017, the Central Bank has introduced new rules for this modality. Therefore, today the rate is valid for only 30 days and can be used once a month.

Many of our readers are looking for institutions that offer the lowest rates. Therefore, we have put together a table with the rates of the main banks on the market.

Banco do Brasil Revolving Credit

Banco do Brasil's revolving credit varies from 13.69% to 2.98% per month, as shown in the table below:

| Credit card | Revolving Interest Rate am |

| Non-providing customers | 12,98% |

| Customers who receive salary or INSS benefits at the bank | 11,98% |

| Ourocard Platinum and Graphite | 10,98% |

| Ourocard Infinite, Black and Nanquim | 8,27 |

| Private Clients | 2,98% |

| Cards with partnerships and Ourocard cards for non-account holders | 13,69% |

| BB Pension | 2,33% |

| Elo Consigned Goldcard | 3,50% |

Nubank Revolving Credit

| Credit card | Revolving interest rate am |

| Nubank Mastercard Credit Card and Ultraviolet Credit Card | 2.75% to 14% |

Bradesco Revolving Credit

| Credit card | Revolving Interest Rates am |

| National Link/Basic International Link/International Link/More Link | Up to 14,99% |

| National Visa/ International Visa/ Visa Gold/ Visa Neo Platinum | Up to 14,99% |

| National Master | Up to 14,99% |

| Amex Green/ Amex Gold Card/ Visa Platinum/ Master Gold | Up to 13.9% |

| Elo Grafite/ Amex The Platinum Card/ Visa Signature/Master Platinum | Up to 12,59% |

| Nanjing Link/Visa Infinite/Aeternum | Up to 9,99% |

| Mastercard Black | Up to 9,99% |

Santander Revolving Credit

Santander already has a revolving credit rate Pre-Fixed 12.21% am. In fact, this value can vary either upwards or downwards – it all depends on each customer’s credit analysis.

On the other hand, Santander customers who receive a salary or salary portability, opting for the Light Account (with service packages above R$$20.00) has a different interest rate.

Currently, the value varies from 3,95%a.m to 9,90% per month, however, the offer is only valid for users of Santander International Credit Card.

Itaú Revolving Credit

Like Santander, Banco Itaú also has a pre-fixed revolving interest credit. Currently, the average is 12,16% per month, but it can change depending on the financial health of each consumer.

The bank's customers can check their personalized rate directly on Internet Banking or the Itaú app. However, if you haven't yet signed up for a card with the bank, the revolving credit is listed in the Membership Agreement. Okay?

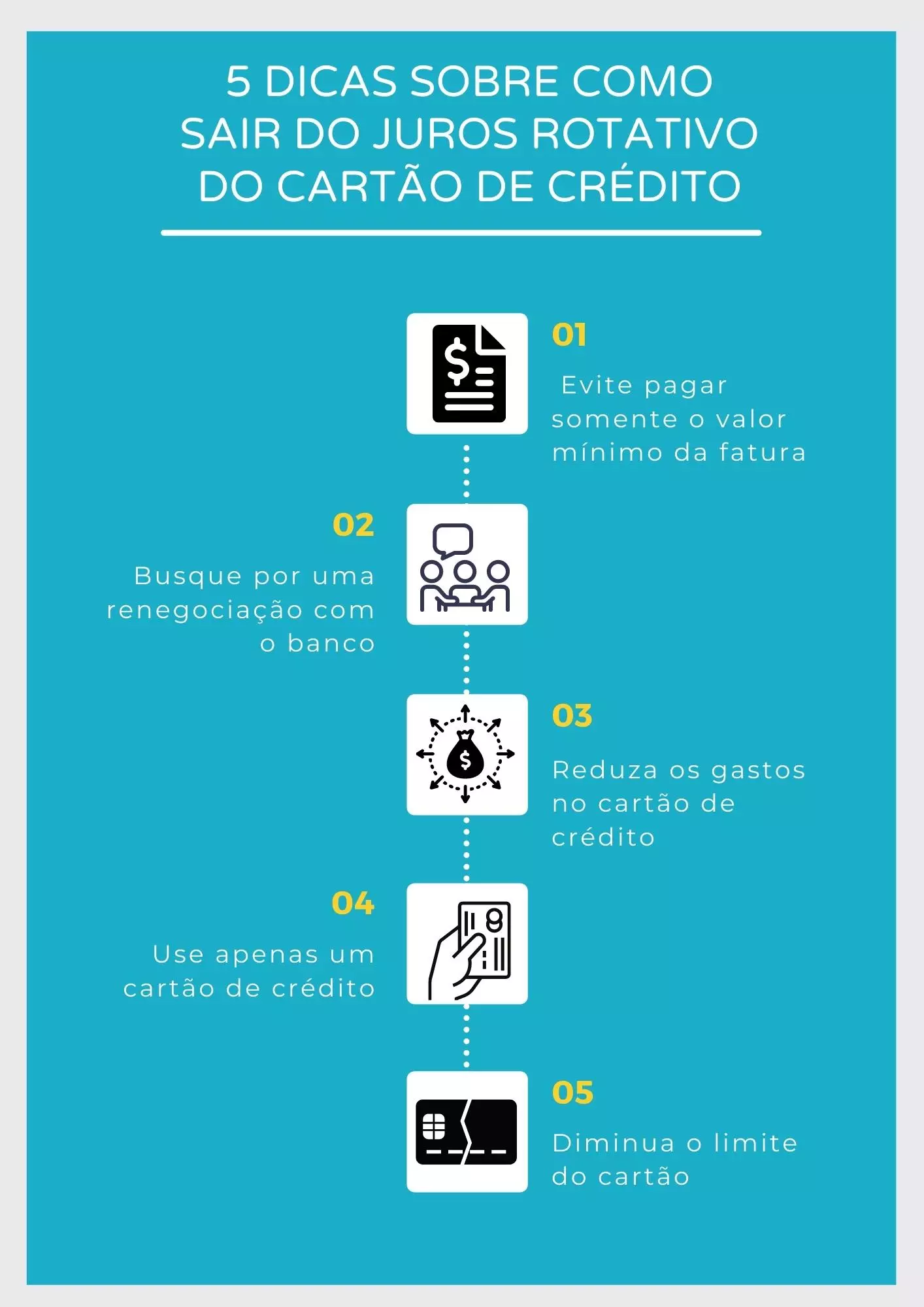

5 tips on how to get out of credit card revolving interest

Now that you understand what this rate is and how it works, let's find out How to get out of credit card revolving interest?

#1 Avoid paying only the minimum amount of the invoice

The first step to avoid falling into the trap of credit card revolving interest is to not pay only the minimum amount on the bill. This is how the consumer is charged this fee, and this is automatic.

One option is to consider paying the bill in installments, but you need to see whether the interest charged is really worth it or not.

#2 Seek renegotiation with the bank

Another solution is to find a way to renegotiate the total debt with the bank, either opting for a installment with fixed interest or payment in cash. In this last case, see if the discounts offered are really advantageous.

Well, in this situation, an advantageous solution is to take out a payroll loan – that credit offered to retirees, pensioners and in some cases CLT employees – have you heard of it?

Interest rates are the lowest on the market, and consumers have a very flexible term to pay their installments.

In fact, in the end, the interest on the loan, when compared to the installment rate on a credit card – plus other charges – is quite reasonable.

To understand more about the subject, read our full article “Consigned Loan – understand what it is”

#3 Reduce credit card spending

Phew, have you managed to negotiate your debt? The next step now is to reduce your credit card debt as much as possible.

In fact, one way to put this into practice is to have self-control when making purchases. We women know that this is very difficult, but if you want to balance your finances and get away from the revolving interest on your credit card, you will need to have this attitude.

So, before buying a certain product or service, check whether it is really a necessity and whether you will have enough income next month to pay off the debt on the due date, ok?

#4 Use only one credit card

A credit card is an essential financial product in your wallet and, by the way, it makes your life a lot easier, as well as increasing your purchasing power, isn't that right?

However, having more than one credit card in your wallet is synonymous with imbalance and this certainly results in losses.

As tempting as it may be, this limit is not your money and we “deceive” ourselves into thinking that if something unexpected happens, it is possible to switch from one card to another and make money from it.

In practice, this is not exactly what happens, and the result is a financial imbalance with huge debts.

So, if you have more than one credit card, it is advisable to cancel the others and keep only one at your disposal.

#5 Lower the card limit

Finally, another important tip for getting out of revolving credit is to reduce your credit limit. After all, if you don't have enough funds to cover your debt on the due date, it means your income isn't enough.

Therefore, reducing the contracted limit will help you both to pay off old debts and to avoid taking on a new outstanding balance.

Remember to always pay in cash and save your credit card for special occasions, such as buying a new refrigerator that you can't afford to pay for all at once.

Conclusion

Based on what was presented in this content, we saw that credit cards are one of the main causes of debt among the Brazilian people. And as if that were not enough, our country's revolving credit is one of the highest in the world.

Therefore, the smartest way out is to watch our spending and avoid paying the minimum amount on the bill as much as possible.

When things get tough, it's common to turn to your credit card, but now you know exactly what happens if you don't have the full amount of money on the bill by the due date.

It is at this point that the fee is charged – therefore, the best option is to opt for installments, or to take out a payroll loan to pay the debt in full.

Did you enjoy learning about revolving credit? Have you ever been in this situation? Leave your comment, we want to hear from you and help you.

Take the opportunity to also discover some options for loans perfect for paying off debts – credit card debts for example. Click the button below and find out all the details.