Advertisements

Consolidated Credit can be the ideal solution for those who have exceeded their credit requirements and now find themselves on the brink of over-indebtedness.

This is because, with this type of credit, you have the possibility of combining several debts into one, which reduces interest and makes debt management easier.

In today's material, we'll talk about this topic, explaining how consolidated credit works, when it's recommended, and other useful information.

Curious? Keep reading!

Consolidated Credit: understand how this option works

Only those who have had more than 5 credit cards know how difficult it can be to keep your accounts in the black.

This is because, although having credit is a positive thing, when it comes from different sources, it can be difficult to reconcile the management and payment of all cards, loans or other forms of credit.

From the expiration date of each contract to the amount and payment methods, it can be a real challenge.

The ideal solution would be to combine everything into a single contract, thus consolidating interest rates, amounts, and payment dates. Much simpler, right?

The good news is that this possibility already exists, and is spreading in Brazil, through the so-called Consolidated Credit.

In this type of credit, you combine your credit agreements into one, in order to unify: interest rate, installment and due date.

This makes debt management much simpler, as well as reducing the incidence of interest.

Can I include all types of credit?

The rules regarding the types of credit that can be consolidated vary according to the guidelines of the financial institution in question.

But, in general, banks do not usually allow consolidation in the following cases:

- Property financing;

- Renegotiated contracts (since negotiations have already been made);

- Credits for legal entities (in this case, banks specializing in companies can provide them).

Therefore, it is easier to find proposals for contracts involving credit cards, personal loans and other related modalities.

However, it is recommended that you always contact the financial institution to check the possibilities in detail.

+This may interest you: Loan to pay off debts: find out if it's worth it!.

Is it worth joining Consolidated Credit?

Consolidated Credit is still a modality that is not very widespread here in Brazil, so little is known about the possibility.

Therefore, it is common to wonder whether or not it is worth joining this modality, but we can help you reach a conclusion.

As we have seen, the main purpose of Consolidated Credit is to prevent customers from getting financially “entangled” with several contracts, offering the possibility of bringing everything together in one.

Furthermore, this option often proves to be more advantageous because it reduces costs, as everything can be more expensive separately.

So, if you are in financial difficulty or believe that your contracts are too expensive, it may be worth joining the Consolidated Credit.

However, it is worth considering that this option is not so common in Brazil, so few institutions offer it.

Furthermore, it cannot be used for all types of contracts, so if you don't have many personal credit contracts, it may not be worth it.

So, evaluate the option carefully to decide whether or not it is worth it, based on your situation.

Which institutions offer this alternative?

If you live in Brazil, you may have difficulty finding financial institutions that offer Consolidated Credit.

This is because this service is not usually part of the group of services offered by the main banks operating in Brazil.

However, if you reside and/or have accounts in Europe or the United States, it may be easier to get proposals.

Tips for joining Consolidated Credit safely and responsibly

As we saw previously, for Brazilians, Consolidated Credit ends up not being an easily accessible alternative.

However, if you live or have bank accounts outside the country, it may be perfectly possible to get good deals.

In this case, it is necessary to take some precautions in order to find safe and truly advantageous proposals.

This is because, one simple mistake and you could end up signing a contract with a scam company, and in addition to not resolving your debts, you could end up with a new contract in your name.

So, here are some tips to avoid this and other similar situations:

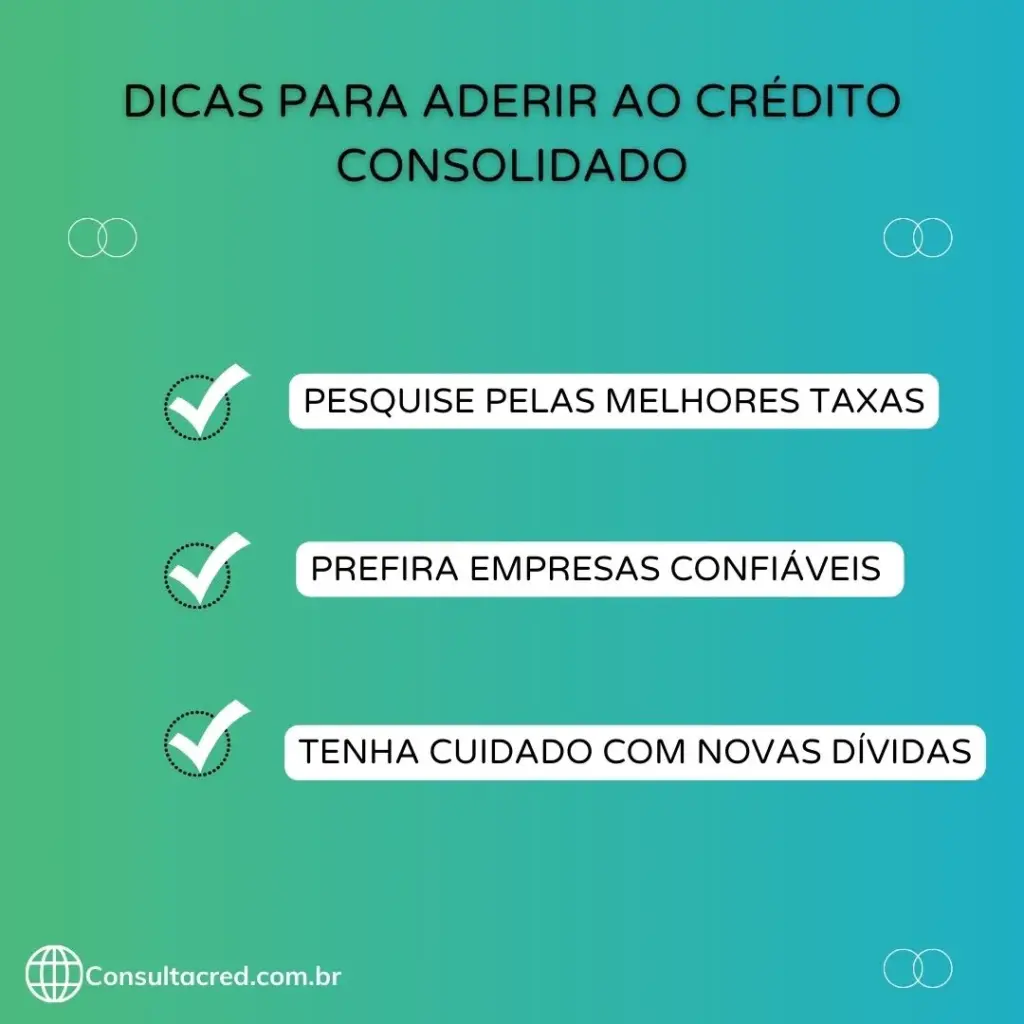

Search for the best rates

Consolidation will only be worthwhile if the new contract's rates are also advantageous. After all, the idea is to reduce expenses, not obtain an even more expensive single contract.

So, do your research to find the best rates on the market that offer you a truly advantageous deal.

Choose reliable companies

As we have already seen, closing the consolidation with an unknown company can represent a great risk.

This is because a scam company can offer you unbeatable conditions, and then disappear, leaving you with all your debts, plus this new contract.

Therefore, research companies that are leaders in this field to ensure your safety!

Be careful with new debts

Many people make the mistake of taking advantage of Consolidated Credit to take on new debts. After all, if I only have one contract now, I can take on more, right?

Although this type of contract actually represents a "bounce" in your monthly budget, taking out more contracts can put you back into over-indebtedness.

And, it may not be possible to reach a new agreement, so this new debt cannot be resolved.

Therefore, after signing this type of contract, avoid new debts as much as possible, for the sake of your financial health.

For more credit-related topics, follow ConsultaCred's content!

+Read also: Special Check: main questions about the service.